Virginia's franchise tax situation is refreshingly simple compared to many other states. The Commonwealth only imposes the Virginia franchise tax on banks and trust companies. No other business entities are subject to this tax.

This clear delineation simplifies compliance planning for organizations managing multiple entity types across different jurisdictions. If your organization includes both financial institutions and other business entities in Virginia, you'll need to prepare bank franchise tax filings for the qualifying banking operations.

Do you owe Virginia franchise tax?

The Virginia franchise tax applies exclusively to banks and trust companies as defined under Va. Code § 58.1-1200. The state's definition includes:

State-chartered banks operating in Virginia

FDIC-authorized national banks conducting business in Virginia

Trust companies operating within the state (includes corporations authorized to exercise fiduciary powers under Virginia banking laws)

The Virginia Department of Taxation provides comprehensive guidance through their Bank Franchise Tax portal to support affected institutions.

Exemptions to the Virginia franchise tax

Several exemptions apply, including banks in active liquidation, savings institutions under different regulatory frameworks, out-of-state banks without physical Virginia presence, and federal land banks.

For specialized financial services companies with complex regulatory structures, verification with corporate counsel or the Virginia State Corporation Commission is recommended before assuming exemption status.

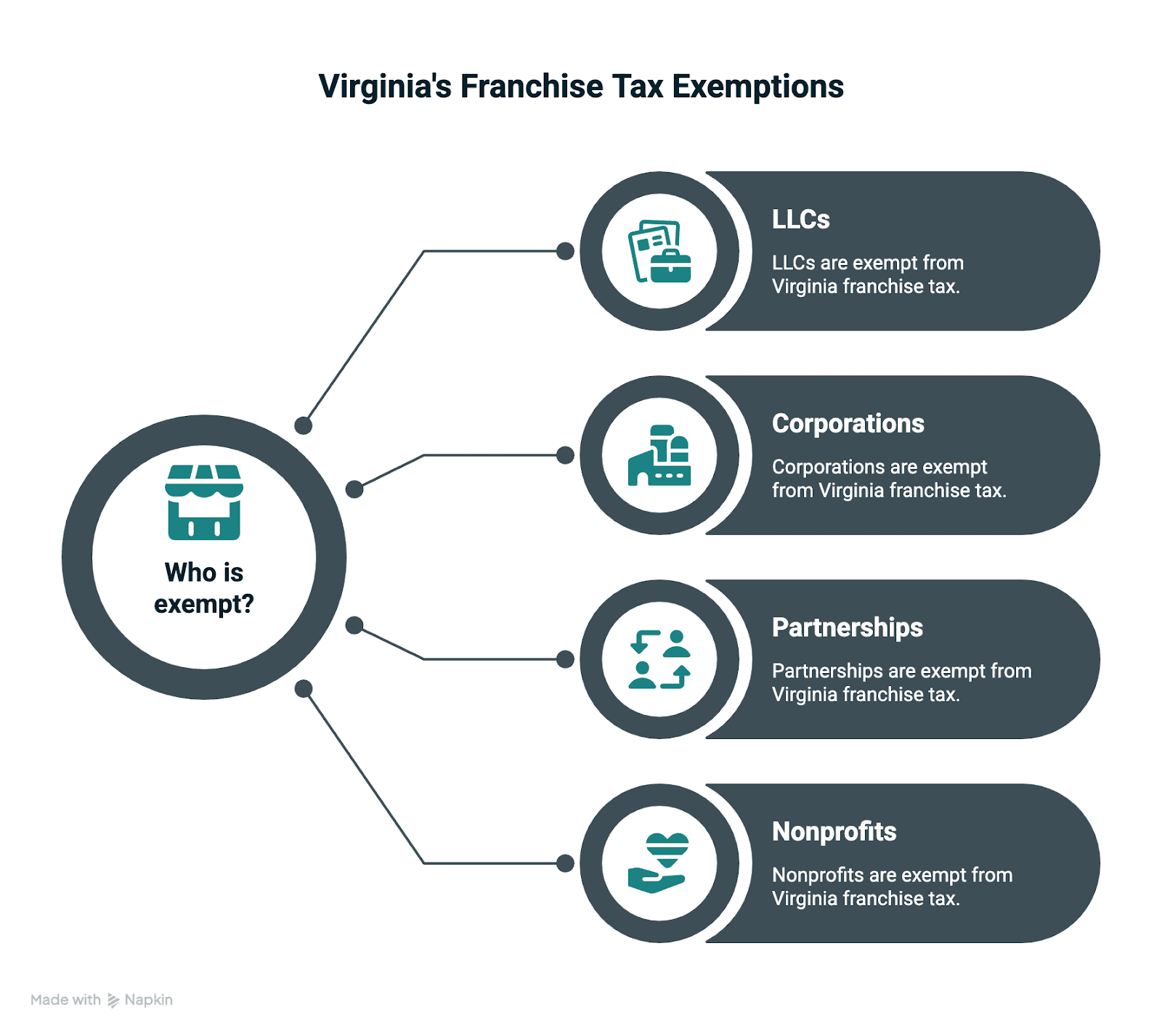

Standard business entities, such as LLCs, corporations, partnerships, and nonprofits, face no Virginia franchise tax obligations regardless of size or industry.

Virginia franchise tax at a glance

Category | Details |

|---|---|

Tax Base | Net capital (equity capital minus goodwill and other intangible assets) |

State Rate | 1% of net capital |

Local Credit | Up to 0.8% of net capital for franchise taxes paid to localities |

Due Date | Return due date: March 1 (automatic filing extension to May 1) |

Payment Due Date | June 1 annually |

Proration | Available for mergers, acquisitions, or mid-year business changes |

E-Filing | Mandatory starting with 2025 tax year returns (due March 1, 2026) |

Credits and late fees

The local credit provision offers significant tax relief, potentially reducing your state liability by up to 80%. For a bank with $50 million in net capital, the maximum local credit could reduce state tax from $500,000 to $100,000, assuming sufficient local franchise taxes were paid during the year.

A 5% penalty applies to unpaid bank franchise tax when returns or payments are late, and interest accrues at the federal underpayment rate plus 2% until paid.

There is a statutory maximum total bank franchise tax liability of $18 million per bank.

Discern helps you track Virginia compliance

Virginia's bank franchise tax applies only to financial institutions and requires specialized tax knowledge for Form 64 filing and net capital calculations.

While Discern does not file Virginia bank franchise taxes directly, Discern can file your Virginia annual reports with the State Corporation Commission, provide registered agent services, notify you when tax obligations are due, and help you track compliance across all your entities.

Ready to simplify your multi-state compliance? Book a demo to see how Discern streamlines entity management across all 50 states and DC.

Published on

2025-12-26

Updated on

2025-12-28