.png)

Utah operates a unified Corporate Income Tax system that combines both income and franchise tax concepts into a single filing obligation. Historically referred to as the "franchise tax," Utah officially calls it the "Corporate Income Tax" for reporting purposes. This integrated approach differs from states that maintain separate franchise and income tax systems.

The tax applies to both domestic Utah corporations and foreign corporations conducting business in the state, with calculations based on federal taxable income allocated to Utah operations through established apportionment formulas.

Who must file?

Utah franchise tax applies to:

C corporations incorporated in Utah

Utah LLCs that have elected to be taxed as C corporations

Utah imposes no minimum income threshold for filing requirements. All applicable corporations must file regardless of income level, including dormant corporations with no business activities. A minimum franchise tax of $100 applies to every C corporation filing Form TC-20, even with zero income.

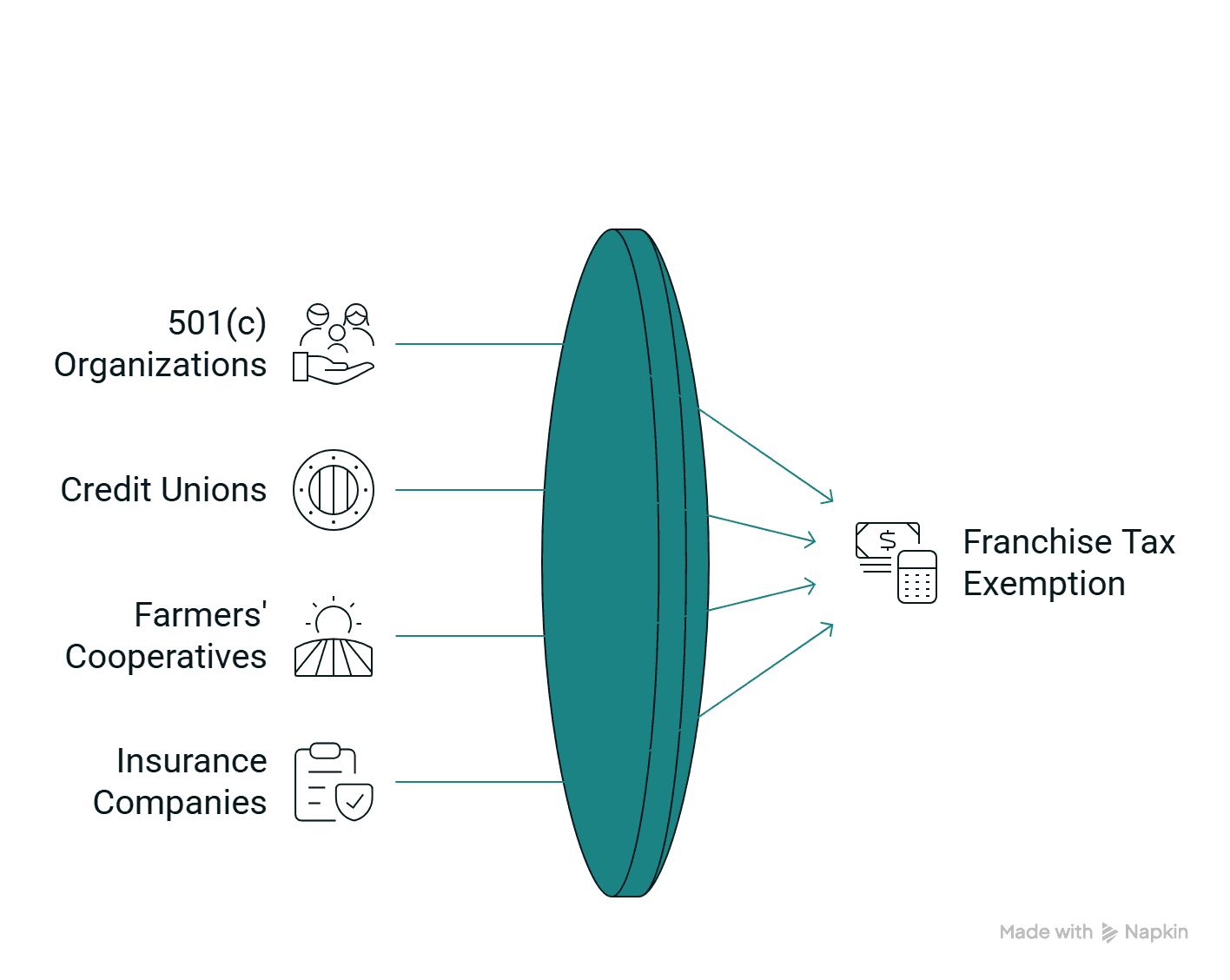

Exemptions to the Utah franchise tax

S corporations generally do not pay Utah corporate income tax on operating income (which passes through to shareholders), but they must file Form TC-20S and may owe tax on certain federal-taxable items such as built-in gains.

Other entities exempt from the Utah franchise tax include:

501(c) organizations (must apply for exemption using Form TC-161)

Insurance companies that pay Utah insurance premium taxes

State and federally chartered credit unions

Certain farmers' cooperatives

Utah franchise tax filing requirements

You don't need a certificate of good standing to file your Utah Corporate Income Tax return, but you still need to file a Utah annual report with the Division of Corporations. There's no separate filing fee for the franchise tax; the cost is just your calculated tax liability.

Additionally, all corporations doing business in the state are required to maintain a Utah registered agent with a physical address in Utah to receive important tax notices and legal documents. Changes to your registered agent must be promptly reported to the Division of Corporations to avoid compliance issues.

Due dates and deadlines

Utah corporations must file their franchise tax by:

April 15 for calendar year filers

15th day of the fourth month after their fiscal year-end for fiscal year filers.

Quarterly estimated payments are required if the expected tax exceeds $3,000, due on April 15, June 15, September 15, and January 15.

Utah offers an automatic 6-month extension to file taxes, moving the deadline to October 15 for calendar year filers. However, tax payments are still due by the original April 15 deadline, even with the extension.

How to file

C corporations use Form TC-20 (Utah Corporation Franchise and Income Tax Return), while S corporations file Form TC-20S. This single form handles both the franchise and income tax components of Utah's unified system.

Electronic filing is available and encouraged through Utah's tax portal, offering faster processing and immediate confirmation.

Utah participates in a joint electronic filing program with the IRS, where federal and state information is submitted simultaneously. Paper filing, on the other hand, remains accepted for smaller entities but requires mailing completed forms to the Utah State Tax Commission.

Starting with 2025 returns, e-filing becomes mandatory for entities with assets exceeding $10 million.

Penalties and compliance

Failure to file Utah franchise tax can result in loss of good standing with the state, potential tax liens and collection actions, and impacts on your ability to conduct business or obtain financing. Late filing triggers escalating penalties:

2% for 1-5 days late

5% for 6-15 days late

10% for 16+ days late (minimum $20 in all cases).

Late payments incur the same tiered penalty structure plus interest at 8% annually for 2025, subject to annual adjustment by the Utah State Tax Commission. Interest compounds daily from the original due date.

Additional penalties include a 10% negligence penalty for substantial understatement, and interest compounds daily from the original due date. Extension filers face a 2% monthly penalty on insufficient prepayments. Even minimal delays trigger penalties, making timely compliance essential.

Additional state taxes

Utah businesses may face other state tax obligations beyond franchise tax, such as:

Sales and use tax

Withholding tax for employees

Unemployment insurance taxes

Property tax on business assets

These taxes have separate filing requirements and deadlines from franchise tax obligations, requiring careful coordination to maintain full compliance.

Streamline your Utah compliance with Discern

While Discern does not file Utah franchise taxes directly, Discern can file your Utah annual reports with the Division of Corporations, provide registered agent services, notify you when tax obligations are due, and help you track compliance across all your entities.

Ready to simplify your multi-state compliance? Book a demo to see how Discern streamlines entity management across all 50 states and DC.

Published on

2025-12-26

Updated on

2025-12-28