Note: the Corporate Transparency Act has had several materials changes since it's initial implementation, and both its rules and enforcement are in flux. Please refer to our latest CTA news for the most up to date information, which supercedes the below.

The Corporate Transparency Act is the widest ranging piece of compliance legislation in recent history. FinCEN estimates it’s going to affect tens of millions of companies this year, and five million a year thereafter.

So how do you actually comply - especially if you have a lot of entities you need to report on?

FinCEN has two main resources here - an FAQ and a BOI Small Entity Compliance Guide. These are long, detailed documents, so we’ve written a simple guide on how to comply:

There are essentially four steps for each company to comply:

Figure out whether your entities are exempt

Determine your Beneficial Owners

Make the initial filing

Update your information if anything changes within 30 days

Figure out whether your entity is exempt

There is a long list of entities that are exempt from filing for the Corporate Transparency Act. When in doubt, refer to your legal counsel on exemption, as for some entities this can be a complex topic.

Some key examples of exempt entities (each of these has specific criteria):

US entities

Investment company or investment adviser

Venture capital fund advisers

Pooled investment vehicle

Large operating company (greater than $5M in annual sales in the US as reported on last years Federal Tax Return, more than 20 full-time employees in the US, AND, an operating presence in the US)

Determine your Beneficial Owners

There are two groups of Beneficial Owners, people who either:

Own or control at least 25 percent of the ownership interests of a reporting company, or

Exercise substantial control over a reporting company

Ownership interests

Owning or controlling at least 25 percent of the ownership interests of a reporting company can be a simple criteria depending on your ownership structure, but importantly this means equity, stock, OR voting rights.

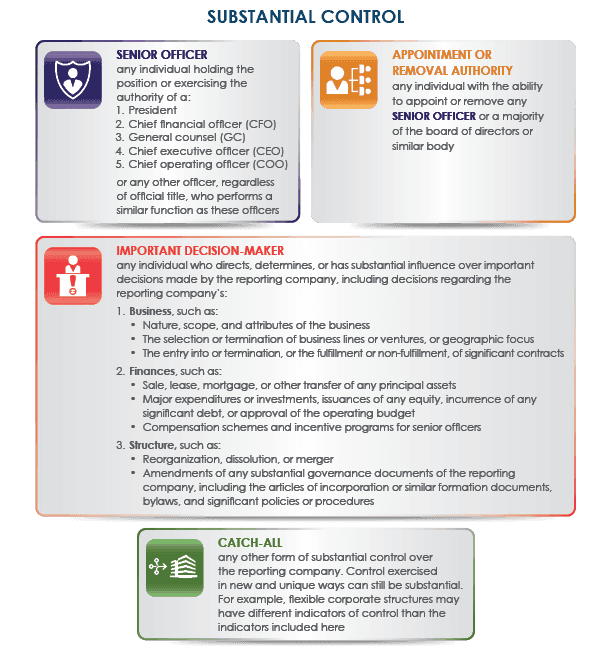

What is substantial control?

Substantial control is fairly wide ranging. It includes everyone at the reporting company who has substantial control, for example:

Senior Officers - C-suite, President, General Counsel, or people that perform these functions regardless of title

Authority to appoint or remove certain officers or a majority of directors of the company

Important Decision Makers - who make decisions on the reporting company’s business, finances, or structure (this often include all members of a board of directors, for example)

Make the initial filing

You’ll need to report information about the Reporting Company itself, as well as personal information about the Beneficial Owners and the Company Applicant.

There are a variety of ways to actually file a Beneficial Ownership report with FinCEN:

File directly with FinCEN, using either their digital portal or their pdf (pdf filing requires Adobe Acrobat).

File via a 3rd party, like Discern.

Update your information if anything changes within 30 days

If any of the information you filed as part of a Beneficial Ownership Information Report changes, you have to file an update report within 30 days. This includes things like adding or removing Beneficial Owners, updating their address information, etc.

How Discern makes filing for the CTA simple

The act of filing for the CTA can require considerable data entry. You could be entering information for several Beneficial Owners, and if you’re doing that for multiple entities, the task is highly repetitive.

With Discern, you’ll enter your data one time. It can then be re-used across any future filings, including for other entities on your account.

Update filings, which are due within 30 days of information change, are also simple on Discern.

In fact, starting next year when you update a piece of information, Discern will automatically prompt you to make update filings where any information has changed.

Even better, there is no per-filing cost on Discern for Corporate Transparency Act filings.

Published on

2025-08-13

Updated on

2025-08-14