.png)

Unlike many states that impose a general franchise tax on businesses, Hawaii stands out by not following this tradition. Instead, the state reserves its franchise tax specifically for certain financial institutions.

Operate a bank, building and loan association, financial corporation, or financial services loan company in Hawaii? You may be subject to this specific tax, as governed under Chapter 241 of the Hawaii Revised Statutes.

For most other businesses in Hawaii, the primary tax obligation is the General Excise Tax (GET). Unlike income taxes levied on profits, GET is a broader tax on gross receipts that impacts nearly all business activities.

The base GET rate is 4% for retailing and most services and 0.5% for wholesaling. Each of Hawaii’s four counties currently imposes a 0.5% county surcharge on activities taxed at the 4% rate, bringing the effective rate on those activities to 4.5% in Honolulu, Maui, Hawaii, and Kauai counties.

Who has to file the Hawaii franchise tax?

If you run a financial institution in Hawaii, you're in a very small club that faces the state's franchise tax. Chapter 241 of the Hawaii Revised Statutes targets banks and a broader group of financial institutions, including:

Building and loan associations

Financial services loan companies

Certain financial corporations

Trust companies

Mortgage loan companies

Each of these entities is required to file a franchise tax return annually.

Regular commercial entities, including C corporations, S corporations, LLCs, partnerships, and sole proprietorships, are off the hook for franchise tax. They face the General Excise Tax (GET) on gross receipts and, for corporations, the state income tax.

Hawaii franchise tax filing requirements

If your organization falls under Chapter 241's definition of a "financial institution," you must comply with Hawaii's franchise tax requirements annually. The state expects comprehensive documentation to verify compliance, centered around Form F-1 but extending beyond just the primary return.

Form F-1 is required to be filed electronically through Hawaii Tax Online, unless the taxpayer obtains a waiver from the Department of Taxation. Hawaii also participates in the IRS Modernized e-File (MeF) program for certain income tax forms, but Form F-1 is filed via Hawaii Tax Online rather than through the federal MeF gateway.

Electronic filing via Hawaii Tax Online results in faster processing and electronic acknowledgement; by contrast, paper returns can take significantly longer to process. For MeF-eligible forms, Hawaii generally issues electronic acknowledgements within two business days.

The tax rate is 7.92%, and Hawaii doesn't charge separate filing fees beyond the tax due, though software vendors may charge licensing fees for their platforms.

Electronic returns filed through Hawaii Tax Online receive electronic acknowledgement from the Department, and MeF submissions generally receive state acknowledgements within a couple of business days.

Paper returns are processed more slowly than electronic filings, and the Department encourages e-filing for faster processing.

Due dates and deadlines

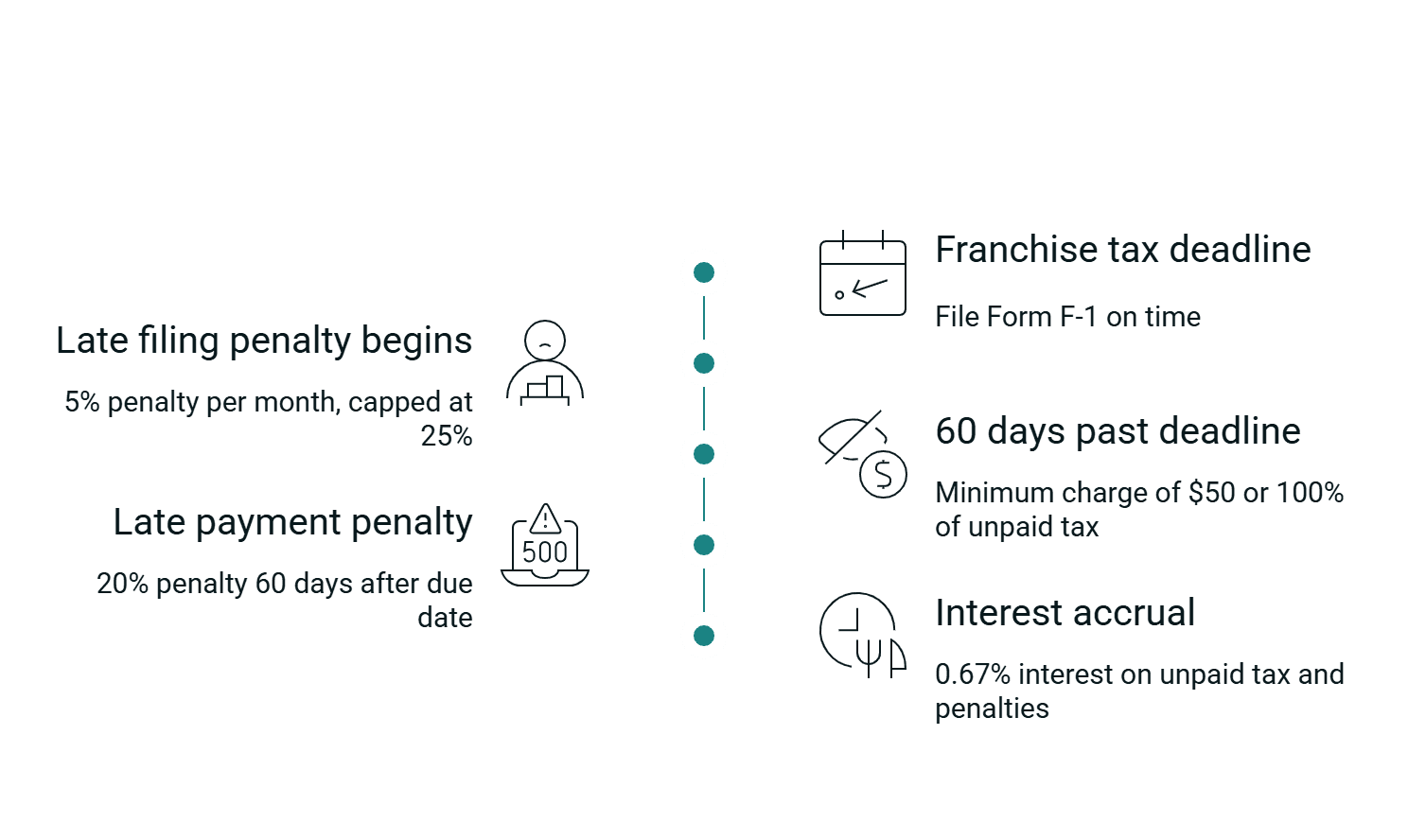

The state gives financial institutions until the 20th day of the fourth month after their taxable year closes to file Form F-1. For calendar-year banks, that's typically April 20.

Payment differs from filing requirements. You must pay the tax by the original due date, but Hawaii lets you spread it across four equal installments: April 20, June 20, September 20, and December 20 for calendar-year filers.

Penalties and compliance

Hawaii's Department of Taxation enforces strict penalties for late franchise tax filings. Miss a deadline and both percentage-based penalties and monthly interest begin immediately, continuing to grow until you pay in full.

File Form F-1 late and you'll face a 5 percent penalty of the unpaid tax for every month (or part of a month) you're behind, capped at 25 percent total.

Filing on time but not paying creates a separate problem. You'll incur a 20 percent late-payment penalty on any tax still outstanding sixty days after the due date. Interest of 2/3 of 1% per month (about 8% per year) applies on unpaid tax and penalties beginning the day after the payment due date and continues until the balance is paid.

Persistent non-compliance can lead to escalating penalties and enforcement actions under Hawaii tax law, which may affect a business’s broader regulatory and contractual relationships.

Additional state taxes

For financial institutions subject to Chapter 241, the franchise tax generally applies in lieu of Hawaii’s corporate income tax and GET on the income covered by the statute. Other activities not covered by Chapter 241 may still be subject to GET or other taxes, but financial corporations are generally exempt from the standard corporate income tax on that income.

Extensions and amendments

Hawaii may grant up to a six-month extension of time to file Form F-1. Taxpayers request this by filing Form N-755; the extension applies to filing only, not to payment.

Any extension applies only to filing. Tax must still be paid by the original due date (April 20 for calendar-year filers). Any unpaid balance begins accruing penalties and interest starting the first day after that due date.

FAQs about Hawaii’s franchise tax

How does Hawaii's franchise tax differ from franchise taxes in other states?

Most states impose a broad "privilege" tax on every corporation, but Hawaii took a different approach. They only impose franchise tax on financial institutions and collect the General Excise Tax (GET) from everyone else.

Do regular corporations and LLCs need to file franchise tax returns in Hawaii?

No. Your regular C corp, S corp, or LLC won't touch Form F-1 unless you're operating a bank, building-and-loan association, or similar financial institution under Chapter 241. You'll handle your state obligations through GET and corporate income tax instead.

If my financial institution operates in multiple states, how is the Hawaii franchise tax calculated?

You'll still file Form F-1, but you only pay tax on the Hawaii portion of your income. The state requires detailed schedules showing how you split gross income and expenses between states, so keep your workpapers organized.

How do I amend a previously filed franchise tax return?

File a fresh Form F-1, mark it "Amended," and include revised schedules with an explanation of what changed. Use the same method you used to file originally and pay any additional tax immediately to avoid new penalties.

Automate your Hawaii and multi-state compliance with Discern

While Discern can't help you with Hawaii franchise tax compliance, our comprehensive compliance management system covers other annual business filings for all 51 U.S. jurisdictions. We also provide deadline tracking and automatic notifications for other Hawaii compliance obligations, ensuring you never miss critical deadlines.

Setup takes just minutes to ensure your business remains compliant across all territories where you operate. Try a Discern demo today.

Published on

2025-12-10

Updated on

2025-12-10